You just finished reading the book, or maybe it is sitting in your Amazon cart. It promises a massive mindset shift that will pull you out of the rat race. Then you run a quick Google search and hit a wall of controversial forum threads. Half the internet calls the author a financial genius; the other half calls him a scammer.

You need to know if you are reading a legitimate financial guide or a well-marketed fable. Let us strip away the marketing hype and look directly at the facts regarding the author, the characters, and whether the financial mechanics hold up in today's economy.

Fact vs. Fiction: Who Is the Real Rich Dad?

The central premise of the book relies on a compelling narrative: Kiyosaki learned how to be an employee from his highly educated but financially struggling biological father (the Poor Dad), and learned how to build wealth from his best friend’s father, an entrepreneur who dropped out of school (the Rich Dad).

For years after the book’s initial publication in 1997, Kiyosaki maintained that the Rich Dad was a real person whose identity had to be kept secret for privacy reasons. As investigative journalists dug deeper and could not find any Hawaii-based hotelier matching the description, the story shifted.

Eventually, Kiyosaki admitted that the Rich Dad is essentially a myth. He is a composite character. Kiyosaki combined the traits, lessons, and quotes from several mentors he had throughout his life into one convenient, father-figure archetype.

Does it matter that the character is fictional? If you view the book as a parable, no. But if you view it as a strict autobiography and a literal roadmap to wealth, the realization that the primary source of the advice never existed in the way described is a massive red flag.

Does it matter that the character is fictional? If you view the book as a parable, no. But if you view it as a strict autobiography and a literal roadmap to wealth, the realization that the primary source of the advice never existed in the way described is a massive red flag.

For a refresh on the core principles taught through this narrative, it can be helpful to review the book's main ideas.

Is Robert Kiyosaki a Fraud? Unpacking the Controversy

When readers discover the fictional nature of the main character, the next logical question arises: is Robert Kiyosaki a fraud?

The answer requires separating his publishing success from his actual real estate and business track record. Kiyosaki is an absolute master of marketing. He built a massive educational empire under the Rich Dad brand. However, his personal business history is riddled with inconsistencies that worry traditional financial advisors.

The Bankruptcy Issues

Kiyosaki has frequently used corporate bankruptcy as a strategic tool, which aligns with his advice on protecting personal assets. In 2012, his company Rich Global LLC filed for bankruptcy after losing a nearly $24 million lawsuit over unpaid royalties to the Learning Annex—the very company that helped promote his early speaking engagements. While his personal wealth was protected, this move drew heavy criticism regarding his business ethics.

The Seminar Upsell Model

A massive portion of the backlash against Kiyosaki comes from the independent seminars bearing his brand name. For years, third-party companies licensed the Rich Dad name to run free seminars across the United States. These free events were often aggressive sales funnels designed to push attendees into buying "advanced" real estate training packages costing upwards of $40,000. Many attendees took on massive credit card debt to afford these courses, only to find the material lacked actionable, local real estate mechanics.

Kiyosaki is not a fraud in the legal sense. He wrote a wildly successful book that changed how millions think about money. But he is a controversial businessman who profits heavily from selling financial education rather than relying solely on the real estate strategies he preaches.

Kiyosaki is not a fraud in the legal sense. He wrote a wildly successful book that changed how millions think about money. But he is a controversial businessman who profits heavily from selling financial education rather than relying solely on the real estate strategies he preaches.

If you are looking for those actual, step-by-step real estate mechanics without attending an overpriced weekend seminar, there are much safer ways to learn the ropes. Before you take on massive credit card debt to learn how to flip properties or generate rental income, consider picking up a comprehensive, strategy-based guide written by someone with a verifiable track record in the industry. It provides the exact blueprints and market analysis techniques that those expensive upsells promise but rarely deliver.

The Millionaire Real Estate Investor

Gary Keller , Dave Jenks , et al.

Rich Dad Poor Dad Review: Does the Advice Actually Work?

To give a fair rich dad poor dad review, you have to split the book into two distinct halves: the psychological framework and the tactical advice.

The Good: The Asset vs. Liability Divide

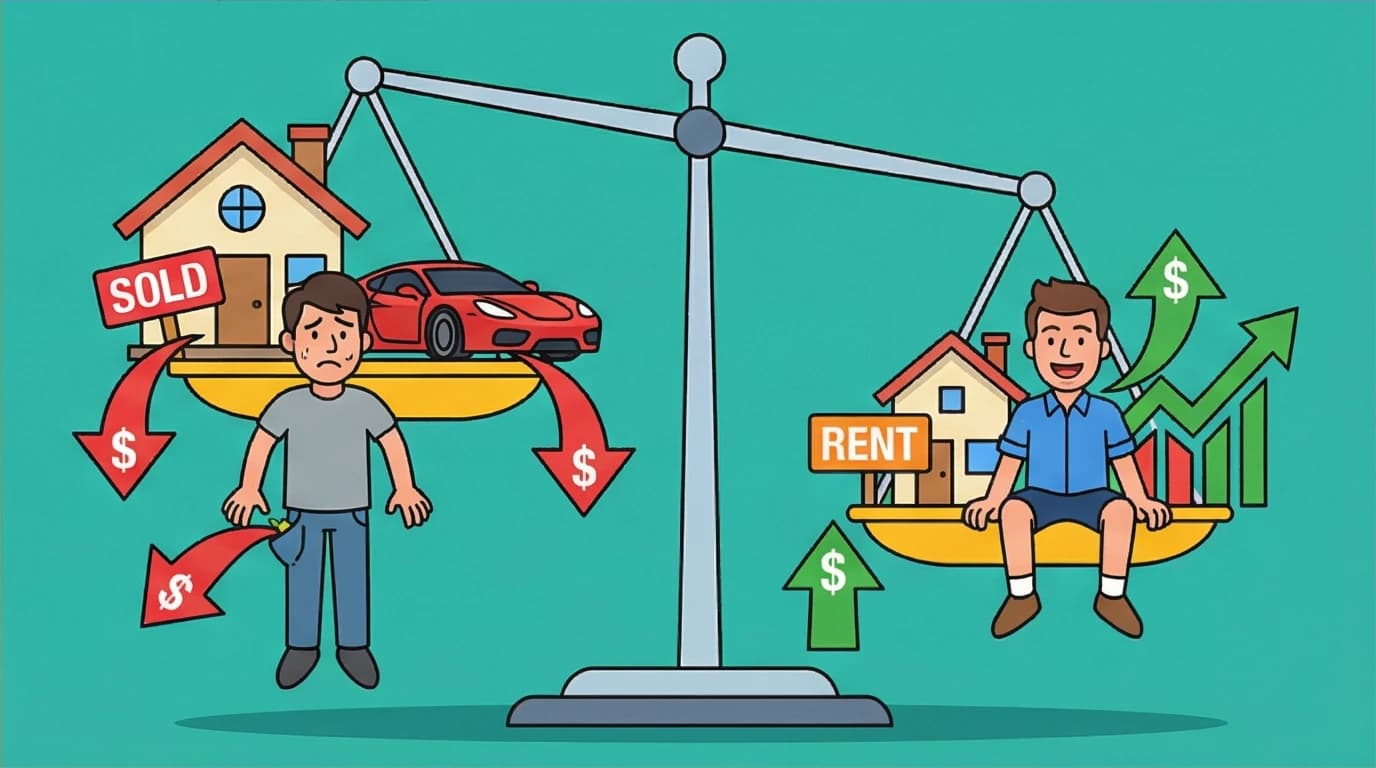

The enduring value of the book lies in one simple, profound concept: The rich buy assets. The poor buy liabilities. The middle class buys liabilities they think are assets.

Kiyosaki redefines these terms outside of strict accounting definitions. In his world:

- An asset puts money in your pocket (rental income, dividends, business profits).

- A liability takes money out of your pocket (car payments, boat loans, and yes, your primary residence).

Telling an American family that their four-bedroom house in the suburbs is not an asset was revolutionary in 1997. It forces readers to realize that a high salary does not equal wealth if every dollar is tied up in paying off lifestyle expenses. This specific mindset shift is highly accurate and remains the single best reason to read the book today.

This single concept is the foundation of Kiyosaki's philosophy for escaping the "rat race."

Kiyosaki is absolutely right that wealth is largely a product of your mindset rather than just your salary. If you want to dive deeper into how our behaviors, biases, and ego impact our financial success, expanding your library beyond technical investing books is a smart move. Understanding the emotional side of spending and saving will reinforce the asset-building mindset and help you avoid the common psychological traps that keep so many high earners living paycheck to paycheck.

The Psychology of Money

Morgan Housel

If building a financial reading list feels overwhelming, or you struggle to find the energy to get through dense books after a long day, a book summary app can be a smart way to absorb these core ideas efficiently.

LeapAhead

Use LeapAhead to get key insights from classics like *The Psychology of Money* and hundreds of other finance books in just 15-minute audio or text sessions.

The Bad: Outdated Tactics and High-Risk Plays

When you move past the mindset and look at the actual mechanics, the rich dad poor dad criticism is entirely justified. The specific tactics Kiyosaki advocates are risky, highly leveraged, and often completely impractical for the average worker.

1. The "Good Debt" Danger

Kiyosaki heavily promotes using "other people's money" (OPM) to buy income-producing real estate. He famously boasts about being millions of dollars in debt because he uses that debt to buy properties that generate cash flow.

Kiyosaki heavily promotes using "other people's money" (OPM) to buy income-producing real estate. He famously boasts about being millions of dollars in debt because he uses that debt to buy properties that generate cash flow.

In the late 90s, or during the zero-interest-rate environment of the 2010s, this worked perfectly. But in an economy with mortgage rates hovering around 7% and inflated housing prices, applying maximum leverage is a fast track to foreclosure. A single unexpected vacancy or a major plumbing repair can bankrupt a highly leveraged beginner.

2. Questionable Tax Advice

The book encourages readers to form corporations to pay for personal expenses with pre-tax dollars. The IRS strictly prohibits using corporate structures to write off personal lifestyle costs. Following his vague tax advice without a licensed CPA is a surefire way to trigger an audit and face massive penalties.

The book encourages readers to form corporations to pay for personal expenses with pre-tax dollars. The IRS strictly prohibits using corporate structures to write off personal lifestyle costs. Following his vague tax advice without a licensed CPA is a surefire way to trigger an audit and face massive penalties.

3. Dismissal of Diversification

Kiyosaki routinely calls mutual funds and 401(k)s a scam designed to steal your wealth. He advises against diversification, pushing instead for concentrated bets in real estate and precious metals. For 99% of the population, a low-cost S&P 500 index fund is the safest, most reliable wealth-building tool available. Telling ordinary people to avoid the stock market in favor of speculative real estate deals is dangerous advice.

Kiyosaki routinely calls mutual funds and 401(k)s a scam designed to steal your wealth. He advises against diversification, pushing instead for concentrated bets in real estate and precious metals. For 99% of the population, a low-cost S&P 500 index fund is the safest, most reliable wealth-building tool available. Telling ordinary people to avoid the stock market in favor of speculative real estate deals is dangerous advice.

If the thought of heavily leveraged real estate and complex corporate tax structures makes your stomach turn, you are not alone. For the vast majority of everyday investors, a slow, steady, and heavily diversified approach in the stock market is the most reliable path to financial independence. If you want a straightforward, stress-free roadmap that favors low-cost index funds over risky property bets, this accessible guide is the perfect antidote to Kiyosaki’s high-risk philosophy.

The Simple Path to Wealth

J.L. Collins

Should You Read It Today?

Yes, but read it as a psychology book, not a finance manual.

If you lack basic financial literacy and want a kick in the pants to stop blowing your paycheck on depreciating items, pick up a copy at Barnes & Noble or download it on Audible. It is incredibly motivating. It will make you look at your bank statement differently.

Do not treat it as a step-by-step blueprint. Once you understand the core concept of cash flow, put the book down and turn to modern, pragmatic resources for actual execution.

For many readers, the next step is finding authors who provide that practical advice.

Despite its flaws and the fictional nature of its central characters, the original text remains a foundational piece of American financial literature. If you go in with your eyes open—viewing it as an incredibly effective motivational tool rather than a literal investment manual—it can completely rewire how you look at your daily spending habits. If you have not yet experienced the mindset shift that millions of others have, it is absolutely worth adding the actual book to your reading list.

Rich Dad Poor Dad

Robert Kiyosaki

And if you want to absorb the book’s core mindset shift without committing to the full read, you can get the main takeaways in a fraction of the time.

LeapAhead

LeapAhead breaks down the essential lessons of *Rich Dad Poor Dad* so you can grasp its powerful asset-building concepts during your commute or coffee break.

FAQ

Is the Poor Dad a real person?

Yes. The "Poor Dad" was Kiyosaki’s actual biological father, Ralph H. Kiyosaki. He was a highly educated man who served as the head of the Hawaii State Department of Education. Despite his steady government salary, he struggled financially, which became the baseline for Kiyosaki's critique of the traditional "go to school, get a safe job" path.

Yes. The "Poor Dad" was Kiyosaki’s actual biological father, Ralph H. Kiyosaki. He was a highly educated man who served as the head of the Hawaii State Department of Education. Despite his steady government salary, he struggled financially, which became the baseline for Kiyosaki's critique of the traditional "go to school, get a safe job" path.

Can I get rich just by reading Rich Dad Poor Dad?

No. The book provides zero actionable blueprints. It will not teach you how to analyze a real estate market, how to structure a business loan, or how to legally file your taxes. It only provides the motivation and the overarching philosophy. You will need practical education and capital to execute the ideas.

No. The book provides zero actionable blueprints. It will not teach you how to analyze a real estate market, how to structure a business loan, or how to legally file your taxes. It only provides the motivation and the overarching philosophy. You will need practical education and capital to execute the ideas.

Why do so many traditional financial advisors hate Robert Kiyosaki?

Financial advisors despise his advice because he actively tells people to avoid saving money and investing in diversified mutual funds. His approach requires taking on massive debt and concentrating risk into single assets like real estate. This "all or nothing" strategy ignores the reality of risk tolerance for normal people.

Financial advisors despise his advice because he actively tells people to avoid saving money and investing in diversified mutual funds. His approach requires taking on massive debt and concentrating risk into single assets like real estate. This "all or nothing" strategy ignores the reality of risk tolerance for normal people.

Is real estate still the best way to build wealth like the book says?

Real estate remains a powerful wealth-building tool due to appreciation and tax benefits, but it is no longer the easy entry point Kiyosaki described in the 1990s. With high interest rates, steep property taxes, and massive down payment requirements, index fund investing has become a far more accessible and liquid way for the average American to build wealth today.

Real estate remains a powerful wealth-building tool due to appreciation and tax benefits, but it is no longer the easy entry point Kiyosaki described in the 1990s. With high interest rates, steep property taxes, and massive down payment requirements, index fund investing has become a far more accessible and liquid way for the average American to build wealth today.